My son is 17year old and he got a w2 for last year(2020). Does he need to file separate tax return for himself? or can he file with us? His W2 is for $3,200

You can still claim him as dependent and he can still file his taxes. The child has to make sure to check the box,Someone can claim You as dependent.

Author: anil Last update: 2022-12-03 01:29

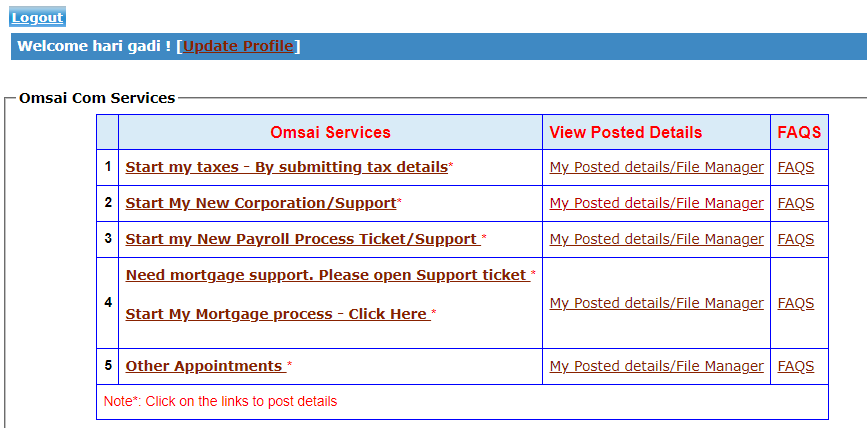

What documents I need to generate Basic Financials.

If new property please bring HUD settlement statement. Please add any other ordinary/necessary expenses not included here.please fill the attached excel sheet

and upload also please.

Author: anil Last update: 2022-12-03 01:36

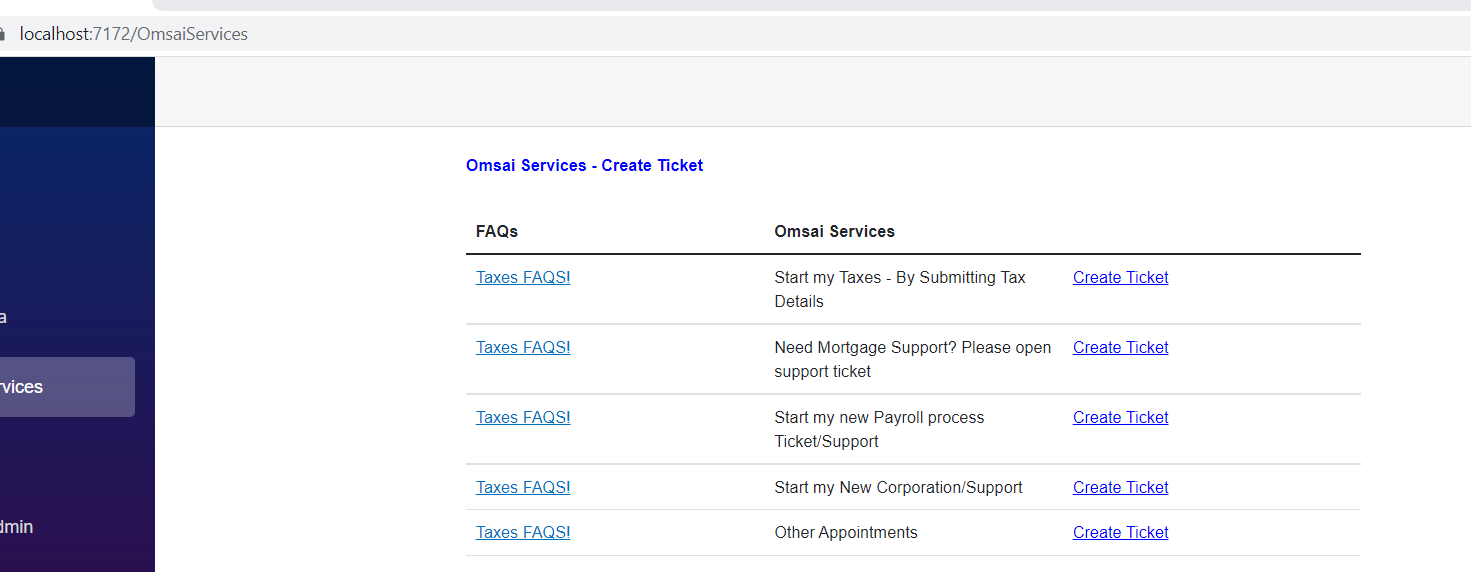

company yearly compliance

A few things are below, please check with your tax preparer for your checklist.

Almost everything you own and use for personal or investment purposes is a capital asset. Examples include a home, personal-use items like household furnishings, and stocks or bonds held as investments. When you sell a capital asset, the difference between the adjusted basis in the asset and the amount you realized from the sale is a capital gain or a capital loss. Generally, an asset's basis is its cost to the owner, but if you received the asset as a gift or inheritance, refer to Topic No. 703 for information about your basis. For information on calculating adjusted basis, refer to Publication 551, Basis of Assets. You have a capital gain if you sell the asset for more than your adjusted basis. You have a capital loss if you sell the asset for less than your adjusted basis. Losses from the sale of personal-use property, such as your home or car, aren't tax deductible.

Short-Term or Long-Term

To correctly arrive at your net capital gain or loss, capital gains and losses are classified as long-term or short-term. Generally, if you hold the asset for more than one year before you dispose of it, your capital gain or loss is long-term. If you hold it one year or less, your capital gain or loss is short-term. For exceptions to this rule, such as property acquired by gift, property acquired from a decedent, or patent property, refer to Publication 544, Sales and Other Dispositions of Assets; or for commodity futures, see Publication 550, Investment Income and Expenses. To determine how long you held the asset, you generally count from the day after the day you acquired the asset up to and including the day you disposed of the asset.

If you have a net capital gain, a lower tax rate may apply to the gain than the tax rate that applies to your ordinary income. The term "net capital gain" means the amount by which your net long-term capital gain for the year is more than your net short-term capital loss for the year. The term "net long-term capital gain" means long-term capital gains reduced by long-term capital losses including any unused long-term capital loss carried over from previous years.

Capital Gain Tax Rates

The tax rate on most net capital gain is no higher than 15% for most individuals. Some or all net capital gain may be taxed at 0% if your taxable income is less than $80,000.

A capital gain rate of 15% applies if your taxable income is $80,000 or more but less than $441,450 for single; $496,600 for married filing jointly or qualifying widow(er); $469,050 for head of household, or $248,300 for married filing separately.

However, a net capital gain tax rate of 20% applies to the extent that your taxable income exceeds the thresholds set for the 15% capital gain rate.

There are a few other exceptions where capital gains may be taxed at rates greater than 20%:

The taxable part of a gain from selling section 1202 qualified small business stock is taxed at a maximum 28% rate.

Net capital gains from selling collectibles (such as coins or art) are taxed at a maximum 28% rate.

The portion of any unrecaptured section 1250 gain from selling section 1250 real property is taxed at a maximum 25% rate.

Note: Net short-term capital gains are subject to taxation as ordinary income at graduated tax rates.

Limit on the Deduction and Carryover of Losses

If your capital losses exceed your capital gains, the amount of the excess loss that you can claim to lower your income is the lesser of $3,000 ($1,500 if married filing separately) or your total net loss shown on line 21 of Schedule D (Form 1040). Claim the loss on line 6 of your Form 1040 or Form 1040-SR. If your net capital loss is more than this limit, you can carry the loss forward to later years. You may use the Capital Loss Carryover Worksheet found in Publication 550, Investment Income and Expenses or in the Instructions for Schedule D (Form 1040) PDF to figure the amount you can carry forward.

Individuals with significant investment income may be subject to the Net Investment Income Tax (NIIT). For additional information on the NIIT. For additional information on the NIIT, see Topic No. 559.

1. upload files after opening ticket. we shall finish all data entry and call you and wrap up the work please.

2. for followup Please send request to my business telegram number 703-496-7483

please add my telegram number's 571-235-4705 (personal) and 703-496-7483(Business).

We are switching to telegram and stopping to use whatsapp soon

https://telegram.org/

give ticket number always please.

Author: anil Last update: 2022-12-03 01:39

Like kind exchange rules

IR-2020-262, November 23, 2020

WASHINGTON â€â€Ã¢â‚¬â€œ Today the Treasury Department and Internal Revenue Service issued final regulations relating to section 1031 like-kind exchanges. These final regulations address the definition of real property under section 1031 and also provide a rule addressing the receipt of personal property that is incidental to real property received in a like-kind exchange.

The 2017 Tax Cuts and Jobs Act (TCJA) limited like-kind exchange treatment to exchanges of real property. As of January 1, 2018, exchanges of personal or intangible property such as vehicles, artwork, collectibles, patents, and other intellectual property generally do not qualify for nonrecognition of gain as like-kind exchanges. Also, like-kind exchange treatment applies only to exchanges of real property held for use in a trade or business or for investment. An exchange of real property held primarily for sale does not qualify as a like-kind exchange.

Under the final regulations, real property includes land and generally anything permanently built on or attached to land. In general, real property also includes property that is characterized as real property under applicable State or local law. In addition, certain intangible property, such as leaseholds or easements, qualifies as real property under section 1031. Property not eligible for like-kind exchange treatment prior to enactment of the TCJA remains ineligible. Neither the TCJA nor the final regulations change whether the properties exchanged are of like kind.

To report a like-kind exchange, taxpayers must file Form 8824, Like-Kind Exchanges, with their tax return for the year they transfer property as part of a like-kind exchange. This form helps taxpayers figure the amount of gain deferred as a result of the like-kind exchange, as well as the basis of the like-kind property received. Form 8824 also helps taxpayers compute the amount of gain they must report if cash or property that isn't of a like-kind is involved in the exchange.

For more information about this and other tax reform changes, visit irs.gov/taxreform.

Caution: The Get Transcript Service is for individual taxpayers to retrieve their own transcripts for their own purposes. Use by any other entities is prohibited.

You can get various Form 1040-series transcript types online or by mail. If you need your prior year Adjusted Gross Income (AGI) to e-file, choose the tax return transcript type when making your request. To find out how much you owe or to verify your payment history, you can view your tax account.

The method you used to file your tax return, e-file or paper, and whether you had a balance due, affects your current year transcript availability. Note: If you need a photocopy of your return, you must use Form 4506.

ÂÂ

Request Online

What You Need

To register and use this service, you need:

your SSN, date of birth, filing status and mailing address from latest tax return,

access to your email account,

your personal account number from a credit card, mortgage, home equity loan, home equity line of credit or car loan, and

a mobile phone linked to your name (for faster registration) or ability to receive an activation code by mail.

Form 8288-B, Application for Withholding Certificate for Dispositions by Foreign Persons of U.S. Real Property Interests

Purpose of form. Use Form 8288-B to apply for a withholding certificate to reduce or eliminate withholding on dispositions of U.S. real property interests by foreign persons, but only if the application is based on:

ÂÂ

Author: anil Last update: 2022-12-03 02:36

Backdoor Roth

A backdoor Roth IRA is a way for people with high incomes to sidestep the Roth's income limits. Basically, a backdoor Roth IRA boils down to some fancy administrative work: You put money in a traditional IRA, convert your contributed funds into a Roth IRA, pay some taxes and you're done.

Author: anil Last update: 2022-12-03 02:49

Backdoor Roth

A backdoor Roth IRA is a way for people with high incomes to sidestep the Roth's income limits. Basically, a backdoor Roth IRA boils down to some fancy administrative work: You put money in a traditional IRA, convert your contributed funds into a Roth IRA, pay some taxes and you're done.

What happens if your income exceeds Roth IRA limits?

What happens if your income exceeds Roth IRA limits?

If your Roth contributions exceed the allowable limit, then those contributions are subject to a six percent excise tax. ... You get your contributions back in full, but your account earnings are subject to the 6 percent excise tax.

For the 2018, 2019 and 2020 tax years, taxpayers must meet the following income requirements to be eligible for the Tuition and Fees Deduction: Taxpayers with a modified adjusted gross income of $65,000 or less ($130,000 if married filing jointly) may claim a maximum $4,000 deduction.

Author: anil Last update: 2022-12-03 03:13

Tax returns where to sign.

example:

Please have your client sign their personal income tax return (1040s) for 2020 and 2019 OR provide their signed IRS e-file Signature Authorization (Form 8879) for the same year(s).

Personal:

Business

example: 1120S

Author: anil Last update: 2022-12-03 03:15

State mailing instruction sample

points.

print state copy and sign

print federal copy and sign.

post state copy followed by federal copy, attach w2 copies.

www.irs.gov for latest rules and regulations please.

The expenses needs to be ordinary and necessary and needs to have receipts and banks statements to s

Author: anil Last update: 2022-12-03 03:18

1099-S sale of real estate

Please make sure if you received 1099-S

Author: anil Last update: 2022-12-03 03:19

H1 Visa fees

Author: anil Last update: 2022-12-03 03:20

Multistates

Generally following things need to be considered

Part year-Part year

Resident/Non Resident

Reciprocal Agreements between states.

Author: anil Last update: 2022-12-03 03:20

5498 IRA

https://www.irs.gov/pub/irs-pdf/f5498.pdf

Form 5498, IRA Contribution Information

Author: anil Last update: 2022-12-03 03:21

Form 1098 Mortgage Interest Statement

Form 1098 Mortgage Interest Statement

Please fill attached excel sheet.

Author: anil Last update: 2022-12-03 03:22

1099-Div Dividends and Distributions

1099-Div Dividends and Distributions

Need to enter all the boxes in which amounts are there, including Qualified dividends etc.

Author: anil Last update: 2022-12-03 03:23

ITIN mailing instructions, IRS appointment

1.tax return binder   print tax return (form 1040 and following pages)  Both spouses have to sign it.   Attach copies of w2  ÂÂ

2. w7 binder  Wife(person who needs itin number) has to sign w7.  ÂÂ

3. one packet for irs office submission  take both tax return copy and w7 binders in one packet to irs office along with originals (passport, marriage certificate, h4 document, H1 document). ÂÂ

Please call IRS and make sure they process w7 and verification of passport etc at the location nearest to you.  Telephone Assistance for Individuals: Toll-Free, 1-800-829-1040 Hours of Operation: Monday – Friday, 7:00 a.m. – 7:00 p.m. your local time (Alaska & Hawaii follow Pacific Time).  Its better to go early in the morning to IRS office along with both binders in one packet. 1.tax return binder2. w7 binder

Type of return. The type of return you file affects the price you’ll pay for preparation. According to the National Society of Accountants, the average fee this filing season for preparing Form 1040 with Schedule A to itemize personal deductions, along with a state income tax return, is a flat fee of $294; the average fee for Form 1040 with the standard deduction, plus a state income tax return, is $188. As you add schedules to your return, the fees increase. For example, the average additional fee for Schedule C for a sole proprietor/independent contractor is $187. The additional fee for Schedule D to report capital gains and losses is $109. The additional fee for Schedule E to report rental income and losses is $136. So individuals whose returns require Schedules A, C, D and E pay an averag

In general, to qualify for the Section 121 exclusion, you must meet both the ownership test and the use test. You're eligible for the exclusion if you have owned and used your home as your main home for a period aggregating at least two years out of the five years prior to its date of sale. You can meet the ownership and use tests during different 2-year periods. However, you must meet both tests during the 5-year period ending on the date of the sale. Generally, you're not eligible for the exclusion if you excluded the gain from the sale of another home during the two-year period prior to the sale of your home. Refer to Publication 523 for the complete eligibility requirements, limitations on the exclusion amount, and exceptions to the two-year rule.

Author: anil Last update: 2022-12-03 03:26

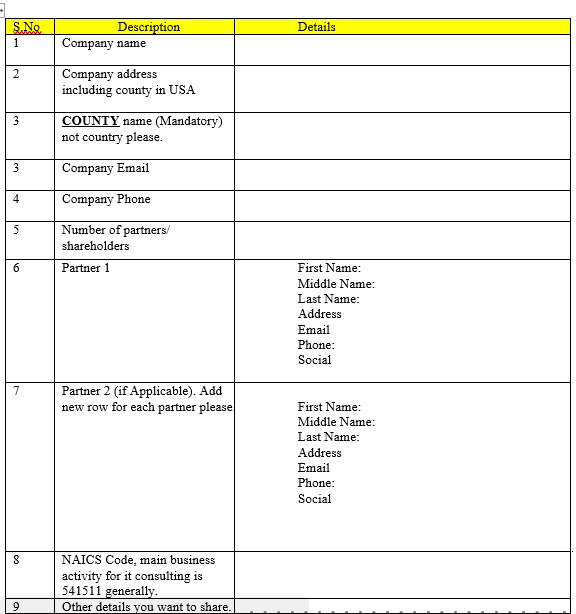

New corp tax filing documents needed

Please give following documents.

1. IRS federal id notice copy

2. If S corp IRS S corp approval notice and 2553 copy

3. State incorporation papers

4. Partners/shareholder details (2553 copy if S corp)

Once you choose to exclude foreign earned income and/or foreign housing costs, you cannot take a foreign tax credit for taxes on income you excluded or could have excluded. If you do, one or both choices may be considered revoked. However, you can choose to take a foreign tax credit on any amount of foreign earned income that exceeds the amounts you excluded under the foreign earned income exclusion and/or the foreign housing exclusion.

Individuals, including sole proprietors, partners, and S corporation shareholders, generally have to make estimated tax payments if they expect to owe tax of $1,000 or more when their return is filed.

Using the Electronic Federal Tax Payment System (EFTPS) is the easiest way for individuals as well as businesses to pay federal taxes. Make ALL of your federal tax payments including federal tax deposits (FTDs), installment agreement and estimated tax payments using EFTPS. If it’s easier to pay your estimated taxes weekly, bi-weekly, monthly, etc. you can, as long as you’ve paid enough in by the end of the quarter. Using EFTPS, you can access a history of your payments, so you know how much and when you made your estimated tax payments.

The 1099-HC form is a Massachusetts tax document which provides proof of health insurance coverage for Massachusetts residents. Every Commonwealth of Massachusetts resident who has health insurance will receive a 1099-HC form. This form is provided by your health insurance carrier and not the GIC.  To download an electronic copy of your Form 1099-HC, you may sign into your medical insurance carrier’s online account, or contact their member services at the number on your ID card for more information.

Author: anil Last update: 2022-12-03 03:51

Corporation

New Corporation documents needed.

Please see attached file.

Author: anil Last update: 2023-01-08 00:20

S corp paper work needed

1. S corp approval copy from IRS and copy of filled 2553 form.

Who May File Form 990-N to Satisfy Their Annual Reporting Requirement?

In general, exempt organizations have an annual reporting requirement although there are exceptions.

Most small tax-exempt organizations that have an annual reporting requirement can satisfy the requirements by submitting Form 990-N, Electronic Notice (e-Postcard.) Form 990-N is submitted electronically, there are no paper forms.

An organization eligible to submit Form 990-N can instead choose to file Form 990 or Form 990-EZ to satisfy its annual reporting requirement.

Small tax-exempt organizations generally are eligible to file Form 990-N to satisfy their annual reporting requirement, if their annual gross receipts are normally $50,000 or less.

Gross receipts are the total amounts the organization received from all sources during its annual accounting period, without subtracting any costs or expenses.

Gross receipts are considered to be normally $50,000 or less if the organization:

Has been in existence for 1 year or less and received, or donors have pledged to give, $75,000 or less during its first taxable year;

Has been in existence between 1 and 3 years and averaged $60,000 or less in gross receipts during each of its first two tax years; and

Is at least 3 years old and averaged $50,000 or less in gross receipts for the immediately preceding 3 tax years (including the year for which calculations are being made).

Note: a subordinate organization in a group exemption that is included in a group return filed by its central organization does not file Form 990-N because the group return satisfies its annual reporting requirement.

All filers must register at IRS.gov prior to filing their next Form 990-N. This is a one-time registration; you won't be asked to register again when filing next year.

Ready to File?

Form 990-N is easy to complete. You'll need only eight items of basic information about your organization.

Form 990-N is due every year by the 15th day of the 5th month after the close of your tax year. You cannot file the e-Postcard until after your tax year ends.

Example: If your tax year ended on December 31, the e-Postcard is due May 15 of the following year. If the due date falls on a Saturday, Sunday, or a legal holiday, the due date is the next business day.

Late Submissions

If we don't receive your submission by the due date, a reminder will be sent to the address on file. Organizations should submit the required form, even if they are late. There is not penalty for late submissions.ÂÂ

While there is no penalty assessment for filing Form 990-N late, organizations that fail to file required Forms 990, 990-EZ or 990-N for three consecutive years will automatically lose their tax-exempt status. Revocation of the organization's tax-exempt status will happen on the filing due date of the third consecutively-missed year.

Search for Form 990-N Filings

To search for organizations that have filed Form 990-N and to view their filings, see Tax-Exempt Organization Search. You can also download the entire database of Form 990-N filings.

Problems Filing

If you experience filing system or website problems, see How to File: Frequently Asked Questions. If you can't fix the problem, call TE/GE Customer Accounts Services at 877-829-5500. A representative will file your Form 990-N information.

File the mandatory biennial (2-year) report to prevent revocation and keep your entity active and in good standing,

Roadmap

In order to keep your entity in good standing with the Corporation Division, a report must be filed within the first year of registration by April 1st and every two years thereafter. To file your biennial report, complete the Biennial Report Form (BRA-25) or submit report filing at CorpOnline. The filing fee for For-Profit entities is $300.00 and $80.00 for Non-Profit entities.

Any profit corporation, limited liability company, limited partnership or limited liability limited partnership annual report filing will have until 12:01 am on May 1, 2021, before a $400 late fee is assessed.

Annual reports are due by the third Friday in September to avoid administrative dissolution.ÂÂ

New Security Alert: An email filing confirmation will be sent to the entity's current email address on file. ÂÂ

3. business tax filing

3 THINGS 1. ANNUAL REPORT 2. Floridarevenue.com/taxes/CITAdditionalinfo 3. FOR LLC PRINT AND POST THE PDF BUSINESS RETURN COPY, S AND C EFILED BY US

Please sample below. please fill 5 details and post to addresss in the form itself. please keep receipt of post.

When to file  File this application on or before the original due date of the taxpayer’s corporate income tax or partnership return. Do not file before the end of the tax year. To file online go to www.floridarevenue.com

The Reciprocal Personal Income Tax Agreement between Pennsylvania and New Jersey means compensation paid to New Jersey residents employed in Pennsylvania is not subject to Pennsylvania income tax

What are the income limits for Medicaid 2020 in Virginia?

Medicaid is now available to Virginia residents earning up to 138 percent of the poverty level. (In 2020, that's about $17,609 for a single person, and about $29,973 for an adult in a household of three people).

Medicaid is the state and Federal partnership that provides medical coverage to eligible needy persons. The purpose of Virginia Medicaid is to improve the health of people in Virginia who might otherwise go without medical care for themselves and their children. There is no enrollment fee or premium for Medicaid coverage if you are eligible. Low co-pays are charged for some Medicaid services.

Who is eligible for Virginia Medicaid?

To be eligible for Virginia Medicaid, you must be a resident of the state of Virginia, a U.S. national, citizen, permanent resident, or legal alien, in need of health care/insurance assistance, whose financial situation would be characterized as low income or very low income. You must also be one of the following:

Pregnant, or

Be responsible for a child 18 years of age or younger, or

Blind, or

Have a disability or a family member in your household with a disability, or

Be 65 years of age or older.

To be eligible, you must have an annual household income (before taxes) that is below the following amounts:

The Clerk’s Office fulfills requests for certified and noncertified copies of business entity documents on file in its office. It also issues certificates of good standing, certificates of fact, and certificates to adjust property title records in circuit courts, which may be needed because of a business entity name change, merger, conversion or domestication.

Certificates - Instant Download The following certificates can be downloaded instantly online via the Clerk's Information System (CIS).

Certificate of Good Standing (Corporations)

Certificate of Fact of Existence/Registration (LLCs)

Certificate of Fact of Existence for VA and Foreign Limited Partnerships

Certified Copies - Instant Download Certified copies of business entity documents filed in the Clerk’s Office are available online for $6.00 per request. There are no additional costs for additional pages when requested through CIS. If all images are available, certified images are done in real time. If any images need to be retrieved by staff, your request will go in-house for fulfillment and be returned by email.ÂÂ

Noncertified Copies - Instant Download Images of various business entity documents filed in the Clerk’s Office are available through the CIS at no charge. For instructions, see the how-to guide for downloading images of business documents.

Images of business entity documents filed on and after January 1, 1997 are generally available. Documents that may have been submitted to the Clerk’s Office but were not accepted for filing or were subsequently withdrawn are not available online to the public.

Conditions of Use

Noncertified copies provided through the CIS are "unofficial" and provided only for public convenience. Images are not to be described or construed as being a certified copy of any document filed with the State Corporation Commission (SCC), or a certification as to the existence or nonexistence of any fact appearing in a document filed with the SCC, or as having the legal effect of any such copy or certification.

The user shall not, expressly or impliedly, state that the reproduction, disbursement, distribution, or preparation of derivative works of the images or the information therein has been done under the authorization of the SCC.

Assessing the accuracy and reliability of an image or information obtained from an image is solely the responsibility of the user. The SCC shall not be responsible or liable for any errors or damages resulting from the use of the image or information.

Paper Copies

To obtain a certificate or a copy of a document by mail, please mail or deliver written request to the Clerk’s Office with a check payable to “State Corporation Commission†for the appropriate fees to:

Mailing Address

Physical Address

Clerk’s Office, State Corporation Commission PO Box 1197 Richmond VA 23218

Clerk’s Office, State Corporation Commission Tyler Building, 1st Floor 1300 E. Main St. Richmond VA 23219

Download the VEC FC-27  (Report to Determine Liability for State Unemployment Tax) and instruction page. (Right click on link, go down to "Save Target As" and save it to your computer). There are several questions on the form regarding the qualifications of General Employers, Agricultural Employers, Household Employers, Nonprofit Employers, acquiring an existing business or if you are already subject to the Federal Unemployment Tax Act (FUTA). Do not mail the form to the VEC until you meet one of the requirements noted in questions 7a through 10 on form FC-27. The VEC will assign an account number only if you meet one of the criteria and mark your response as "yes".

Mail your completed VEC FC-27 form Virginia Employment Commission Employer Accounts P.O. Box 26441 Richmond, VA 23261-6441

An image is a backup copy of your Servers. You can restore your Server by installing an image. You can also use an image to set up another Server as a clone of the first one. With a backup plan, you can have images created automatically at regular, scheduled intervals.

Please fill the attached real estate schedule if you own multiple properties please.

ÂÂ

Author: anil Last update: 2022-12-12 07:33

Gift Letter

Please find the attached documents.

Gift Letter & Requirements

Step 1: The person giving you your gift, the Donor, must complete and sign the “Gift Letter†below. Your signature is also required.

Step 2: Additional Donor Requirements - Source of gift funds - provide the following: ·        A copy of the gift check OR wire transfer form showing gift amount transferring out of account ·        A copy of the bank statement showing gift withdrawal OR a bank printout that is stamped and signed by the bank showing gift withdrawal ·        A copy of the bank statement showing gift funds clearing as well as a 30 day history prior

Step 3: Additional Client Responsibilities - Transfer of gift funds - provide the following: ·        A copy of the bank statement showing the gift being deposited with the funds showing as available in the balance

Author: anil Last update: 2022-12-12 06:07

Mortgage paid by Business can be excluded from DTI

Author: anil Last update: 2022-12-05 03:54

Secondary home rules from one major lender

Author: anil Last update: 2022-12-05 04:34

it's my responsibility to ensure you have a clear and clean title prior to your closing. Please review the following information from title and advise We have been advised that the client would like to add her husband to the title. We need to know how they would like to hold title? Here are the choices: JTWFROS Joint Tenants Tenants in Common Community Property CP with Right of Survivorship Please let me know. Thank you,

Author: anil Last update: 2022-12-05 04:35

one 6 months rule

Thank for you taking my call. As I stated this file has no mortgage currently and was purchased 1 month ago. The rate/term would be adding a mortgage to a property that has no mortgage. That is at no benefit to the client. Here are the guidelines. The client would need to come back once he reaches 6 months on title seasoning. Client Eligibility ID x103284 If at least one client has been on title greater than or equal to 6 months prior to closing, cash out is allowed.

Author: anil Last update: 2022-12-05 04:35

Closing costs:D plus E minus lender credits calculation

Author: anil Last update: 2022-12-05 04:36

Amrock Details

Please find details for each state

Author: anil Last update: 2022-12-06 07:11

Rental passive losses while refinancing.

Please see attached pdf file.

Author: anil Last update: 2022-12-06 05:57

Pricing information: please send 10 details.

Pricing Info Template

1.Rate & Term or Cash Out

2. Monthly Income

3. Property Value

4. Loan Amount

5. Average Credit Score

6. property addess, Zip code / State / county

7. Second mortgage or HELCO?

8. Property Type (Single family home or condo)

9. Term (#years)

10. Investment property or Primary home?

Author: anil Last update: 2022-12-06 01:12

good website to check average rates in the market.

(Don't submit application at provident only check rates please to get an idea)

For average rates please above website is good indicator of average rates yours could be higher/lower depending on FICO scores loan to value ratio, zip code etc.

Property: Processor Assist: Provide proof that the project has an active Fidelity/Employee crime policy with coverage equal to or greater than the amount of HOA dues collected by the HOA from the project over a 3 month period. Project Review .

ÂÂ

What is Crime and Fidelity Insurance? Crime and Fidelity Insurance protects the actual money the Association has in the operating account and reserve accounts. Crime and Fidelity Insurance protects the money from embezzling, check fraud, invoice padding or false invoices, computer fraud and wire fraud.

Author: anil Last update: 2022-12-06 01:31

When changing term please give rate also.

New term (15, 20 or 30 etc)

New rate

Author: anil Last update: 2022-12-06 01:38

Loan Recast

Some information about recast, please check new rules and regulations always please.

ÂÂ

Author: anil Last update: 2022-12-06 01:39

Appraisal appeals

You can fill below details and send to the appraisal company.

Property: Processor Assist: Provide proof that the project has an active Fidelity/Employee crime policy with coverage equal to or greater than the amount of HOA dues collected by the HOA from the project over a 3 month period. Project Review .

ÂÂ

What is Crime and Fidelity Insurance? Crime and Fidelity Insurance protects the actual money the Association has in the operating account and reserve accounts. Crime and Fidelity Insurance protects the money from embezzling, check fraud, invoice padding or false invoices, computer fraud and wire fraud.Jul 21, 201

Fidelity/crime insurance is required for certain condo and co-op projects.

The HOA or co-op corporation must have blanket fidelity/crime insurance coverage for the dishonest or fraudulent acts of anyone who either handles or is responsible for funds held or administered for the HOA or co-op corporation, whether or not that individual receives compensation for services. Accordingly, the HOA or co-op corporation policy must include coverage for the acts of any management agent. The insurance policy must name the HOA or co-op corporation as the insured and the premiums should be paid as a common expense by the association or corporation.

A management agent that handles funds for the HOA or co-op corporation should additionally be covered by its own fidelity/crime insurance policy.

ÂÂ

Exceptions to Fidelity/Crime Insurance Requirements

Fidelity/crime insurance is required for all condo and co-op projects, with the following exceptions:

condo or co-op projects consisting of 20 units or less, or

condo or co-op projects that would need fidelity/crime insurance coverage of $5,000 or less (based on the calculations described in Amount of Coverage below).

ÂÂ

Note: In states that have statutory fidelity/crime insurance requirements, Fannie Mae accepts those requirements in place of its own.

ÂÂ

ÂÂ

Amount of Coverage

The HOA or co-op corporation policy must cover the maximum funds that are in the custody of the HOA or co-op corporation or its management agent at any time while the policy is in force. Fidelity/crime insurance is not required if the maximum estimated funds are less than or equal to $5,000.

A lesser amount of coverage is acceptable if the project’s legal documents require, or another source acceptable to the seller/servicer verifies, that the HOA or co-op corporation and any management company adheres to one or more of the following financial controls:

Separate bank accounts are maintained for the working account and the reserve account, each with appropriate access controls, and the bank in which funds are deposited sends copies of the monthly bank statements directly to the HOA or co-op corporation.

The management company maintains separate records and bank accounts for each HOA or co-op corporation that uses its services, and the management company does not have the authority to draw checks on, or transfer funds from, the reserve account of the HOA or co-op corporation.

Two members of the Board of Directors must sign any checks written on the reserve account.

Even then, the fidelity/crime insurance coverage must equal at least the sum of three months of assessments on all units in the project, unless this calculated amount is less than or equal to $5,000, in which case fidelity/crime insurance is not required.

ÂÂ

Cancellation/Modification Requirements

The policy must require at least ten days’ written notice to the HOA, co-op corporation, or insurance trustee before the insurer can cancel the policy.

ÂÂ

Author: anil Last update: 2022-12-06 01:44

Mortgages » Mortgage Conditions

County taxes bills/receipts

Please go to your county website and download the tax files

Please call your present mortgage company and ask them for payoff statement till 1 month (30 days from now) and ask them to fax to us 703-997-8857

Author: anil Last update: 2022-12-06 01:45

New home purchase details needed

Please find the attached word document

Author: anil Last update: 2022-12-06 01:46

Tax returns where to sign.

example:

Please have your client sign their personal income tax return (1040s) for 2020 and 2019 OR provide their signed IRS e-file Signature Authorization (Form 8879) for the same year(s).

Personal:

Business

example: 1120S

Author: anil Last update: 2022-12-06 01:47

Earnest money condition

Please provide an asset statement for the account from which the earnest money deposit check was written or the wire transfer funds originated. The statement must show 30 days of transaction activity prior to and including the deposit clearing your account. If your most recent monthly statement doesn't include the deposit, please also provide the transaction history through the date the deposit cleared. We need to verify the origin of the funds from your earnest money deposit check or wire transfer. Please note the following: Bank statements should include your name, bank name and account number. Include all numbered pages - even blank pages. Statements must show a beginning and ending balance. Online statements must contain the bank's valid website address.

Underwriting: Please provide proof of earnest money deposit check/wire, proof of earnest money deposit check/wire has cleared, and proof of 30 day activity prior to earnest money deposit clearing.

Also statement from your settlement agent informing that earnest money has cleared.

Author: anil Last update: 2022-12-06 01:47

Conditions mortgage loan

Please send the following documents asap.

If not applicable to your case please ignore.

Author: anil Last update: 2022-12-06 01:48

Bank statements

Bank statements.

Name of account holders

account numbers.

however, we are unable to use the Asset statement in this format as it does not list the asset account holder name(s). Please resend the most recent statement, all pages that list the Account number, and the name(s) of the account holder(s). Thank you!

Hello All,As you all know Employers seeking to file H1B Cap subject petitions for the  Fiscal Year 2022 Cap must first electronically register and pay the associated $ 10.00 H1B registration fee. We have started the process of collecting documents for H1B registration and the forms and retainer agreements are attached herein. Once the Beneficiary is selected in the H1B Cap lottery you have to submit the list of documentation required for submission of H1B packet along with our regular fee fixed for the H1B Petitions. Please call us if you have any doubts.Yours Truly,Bindu Sanjeevkumar, esq.Law Offices of Bindu Sanjeevkumar, PCEmail  bindukumar@bindulaw.comMobile +1 (908) 962 8889Office  138 West 25th St., 10th floor, New York, NY Every alien - a temporary worker, visitor, student, child or permanent resident - is required to report address changes (residential) to the USCIS using Form AR-11. Complete it on-line or mail the AR -11 formsÂÂ

ÂÂ

Author: anil Last update: 2022-12-05 03:06

FHA Loans

FHA loan 6 months employment condition for one lender

Please choose one of the following options to log in to New Jersey's Corporation Business Tax filing and payment service. (Before using this service, your business must already be registered with the State of New Jersey.)

ÂÂ

1.

File Extensions, Pay, and Access Past Payments: Log in below using the first prompt. Enter your taxpayer identification number* and Personal Identification Number (PIN). Your PIN is printed on the Welcome Letter you received after registering your business. If you use this option, you can file extensions and pay taxes and view information on past payments. If you don't know your PIN or need other information, call the Division of Taxation at 609-292-6400. To obtain a PIN, you will be asked to supply identifying information from previous business tax filings.

ÂÂ

2.

File Extensions and Pay Taxes Only: This option allows you to file extensions and pay taxes only. You can't view information on past payments. Log in using your New Jersey tax identification number* and business name. Call the Division of Taxation at 609-292-6400 if you need help or have questions.

ÂÂ

3.

Sign Up for Premier Business Services (PBS). This comprehensive account service allows you to create your own Login ID and Password to access multiple business services, including filing New Jersey tax returns and wage and corporate reports, paying taxes, and viewing information on past filings and payments.

ÂÂ

* Your New Jersey tax identification (ID) number has 12 digits. If you have a Federal Employer Identification Number (FEIN) assigned by the Internal Revenue Service (IRS), your New Jersey tax ID number is your FEIN followed by a 3 digit suffix. If you do not have a suffix, enter three zeroes. Do not use hyphens, slashes, or other punctuation. (Example: If your FEIN is 12-3456789, enter 123456789000). If you do not have a FEIN, your New Jersey tax ID number is usually the Social Security Number of the primary business owner followed by three zeroes.

Author: anil Last update: 2022-12-05 03:16

Texas

Texas webfile number

you should receive letter from Texas, please see sample below.

PUBLIC INFORMATION AND OWNER INFORMATION REPORTSFranchise Tax

Taxpayer: The information listed is the Taxpayer Name, Taxpayer Number and Secretary of State (SOS) File Number or Comptroller File Number on file for this entity.

Mailing address: Mailing address on file for this entity.

Principal Office

Principal Office: Enter the address within the United States where the entity’s records are kept.

Principal Place of Business: Enter the address of the place of business for day to day operations.

Officers, Directors, Managers: Enter the name, title, term expiration date and complete address for each officer, director, member, general partner or manager of the corporation, LLC, limited partnership, professional association or financial institution as of the date the report is filed. If you need to add more Officers, Directors and/or Managers choose Add Another.

Note: For reports due prior to 2016, Limited Partnerships (LP) and Professional Associations (PA) were required to file the Ownership Information Report.

If the information is prepopulated already, this information is obtained from the most recent Public Information Report (PIR) processed by the Secretary of State. If the information is not correct, please edit the information. We will provide the Secretary of State with this updated information.

Domestic profit corporations and domestic professional corporations must enter all officers, which must include the president and secretary, and all directors. One person may hold all offices.

Domestic non-profit corporations must enter all officers. Different persons must hold the offices of president and secretary. There is a minimum of three directors.

Domestic limited liability companies must enter all managers and, if the company is member-managed, list all members. All officers, if any, must be listed.

Non-Texas entities must enter all officers and directors that are required by the laws of the state or country of incorporation or organization.

Limited partnerships must include all general partners.

Professional associations should report the members of their executive committee.

Owned Entity(s): Enter information for each (subsidiary) corporation, LLC, LP, PA or financial institution, if any, in which this entity owns an interest of 10 percent or more. If you need to add more choose Add Another.

Owned By, Corporation: Enter information for each (parent) corporation, LLC, LP, PA or financial institution, if any, that owns an interest of 10 percent or more in this entity. If you need to add more choose Add Another.

Registered Agent: Enter the name and address of the registered agent/office.

Declaration Statement: Check the box to declare that the information in this document is true and correct to the best of your knowledge and belief, as of the date filed, and that a copy of this report has been mailed to each person named in this report who is an officer, director, member, general partner or manager and who is not currently employed by this or a related corporation, LLC, LP, PA or financial institution. The Declaration Statement must be checked to continue.

Need assistance?

If your question is not addressed here, contact us.

n S corporation is a corporation that elects to be taxed as a pass-through entity. Income, losses, deductions, and credits flow through to the shareholders, partners or members. They then report these items on their personal tax return. IRS approval is required for the S election status.

Some key features of S corporations are:

They do not pay federal income taxes

They’re limited by the types of owners (shareholders) and cannot exceed 100 shareholders

A separate bank account and separate records are required with this form of business

S corporations are subject to the annual $800 minimum franchise tax

Registered to do business in California with the Secretary of State

Receiving California source income

You should use the below guidelines to file your state income taxes:

We tax every S corporation that has California source income 1.5%. Visit our tax rates table for complete list of tax rates

Your minimum franchise tax ($800) is due the first quarter of each accounting period

You must pay the tax whether your corporation is active, inactive, operates at a loss, or files a return for a short period (less than 12 months)

We waive the minimum tax on newly formed or qualified S corporations filing an initial return for their first taxable year if both of the following are true:

They did not conduct any business in California during the tax year

Their tax year was 15 days or fewer

Any first-year net income is still subject to the 1.5% tax rate

Pay Online Paying online is convenient, secure, and helps make sure we get your payments on time. Please visit our secure site ATAP (Arkansas Taxpayer Access Point) at www.atap.arkansas.gov

. ATAP allows taxpayers or their representatives to log on, make payments and manage their account online.

ÂÂ

Deadline & Extensions

The due date for filing your Arkansas Individual Income Tax return is April 15. If April 15 falls on a weekend or a holiday, your return is due on the next business day. If you file a federal or State of Arkansas Extension and you file your return before the deadline, you will not be charged for any late filing penalties for filing the tax return past the original due date. Interest and any applicable failure to pay penalty will be charged on all tax due returns from the original due date until the date you file the income tax return.

If you have already filed a federal extension, you do not have to file a state extension. The State of Arkansas will honor an accepted federal extension and your due date will be the same as the federal return. You will need to check the appropriate box on the front of your Arkansas return when you file.

Note: If you file an Application for Automatic Extension of Time (Federal form 4868), you will not receive an approved copy back from the Internal Revenue Service. You will need to check the appropriate box on the front of your Arkansas return when you file.

If you want to file specifically for a State of Arkansas Extension, you must file Arkansas Form AR1055. This form must state a reason for the extension and be postmarked on or before April 15. Inability to pay will not be honored as a valid reason for an extension of time to file.

The federal and State of Arkansas extensions will extend the time to file your tax return 180 days or October 15th for calendar year filers.

Author: anil Last update: 2022-12-05 03:20

Maryland

Maryland to get refund of taxes withheld (including sale of property)

MARYLAND NONRESIDENT INCOME TAX

In addition to the Nonresident Withholding Tax, the owner is also required to file an income tax return with Maryland for the year in which he or she sold the Maryland property.ÂÂ

Author: anil Last update: 2022-12-05 03:20

Maryland tax withheld non resident real estate sales

An accredited investor is a person or a business entity who is allowed to deal in securities that may not be registered with financial authorities. They are entitled to such privileged access if they satisfy one (or more) requirements regarding income, net worth, asset size, governance status or professional experience. In the U.S., the term is used by the Securities and Exchange Commission (SEC) under Regulation D to refer to investors who are financially sophisticated and have a reduced need for the protection provided by regulatory disclosure filings. Accredited investors include natural high net worth individuals (HNWI), banks, insurance companies, brokers and trusts.

hould match bank deposits.

hould match bank deposits.

ÂÂ

ÂÂ